Upcoming Event

Free Newsletter

Free Newsletter

Redlining history linked to COVID-19 prevalence

Redlining history linked to COVID-19 prevalence

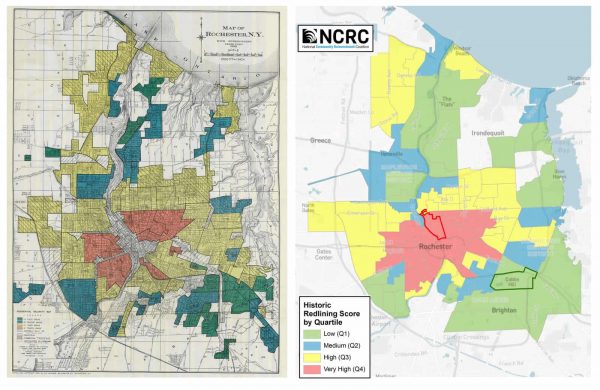

Less than a century ago, the Home Owners Loan Corp., a now-defunct federal agency, went into neighborhoods nationwide to map them in order to inform the government on the default risk for loans they wanted to purchase from banks.

The Federal Housing Administration sanctioned “redlining,” literally the act of drawing a red line around neighborhoods deemed undesirable for home mortgage loans. Underwriting guidelines of the FHA stipulated that neighborhood stability and the presence of “incompatible racial and social groups” were elements that should be considered during the appraisal and assessment process for qualifying mortgage lending.

“They found segregation that was already in place, populations, especially African Americans, which were typically confined to certain areas of the city, either by practice or by local law,” said Jason Richardson, director of research and evaluation for the National Community Reinvestment Coalition. Richardson last month joined several speakers in the NCRC’s Just Economy webinar series “Redlining and Neighborhood Health,” which featured a segment on redlining in Rochester.

“HOLC had the effect though of essentially codifying that segregation and reinforcing it by encouraging banks not to lend in redlined areas,” Richardson explained. “And they did that by making it clear they weren’t going to buy loans in redlined areas.”

From a bank’s point of view, a loan to someone living in a redlined area was a lot more dangerous.

“Not only was it probably going to be a loan with a higher risk of default, according to them, they also knew that they would not be able to sell that loan,” Richardson added. “So the segregation existed; the federal policy amplified it and essentially trapped it in amber for the next 40 years until it was eventually made illegal in the late 1960s to redline neighborhoods in this way.”

But the damage was already done.

Richardson co-authored a new report from NCRC that found that today, those same neighborhoods suffer not only from reduced wealth and greater poverty, but from lower life expectancy and higher incidence of chronic diseases that are risk factors for poor outcomes from COVID-19.

“The Lasting Impact of Historic ‘Redlining’ on Neighborhood Health: Higher Prevalence of Covid-19 Risk Factors” found that:

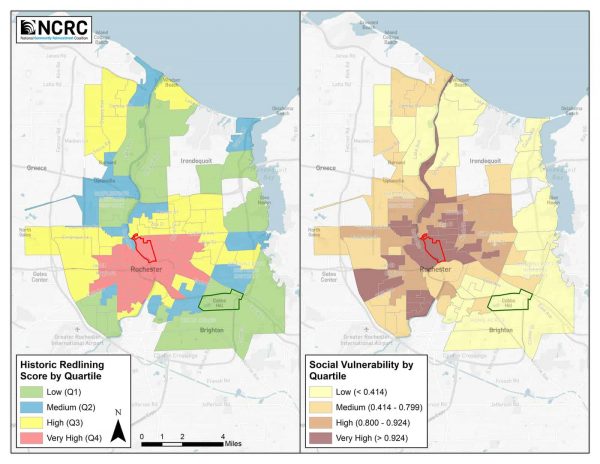

- Greater historic redlining is related to current neighborhood characteristics, including increased minority presence, higher prevalence of poverty and greater social vulnerability.

- There are statistically significant associations between greater redlining and general indicators of population health, including increased prevalence of poor mental health and lower life expectancy at birth.

- There are statistically significant associations between greater redlining and preexisting conditions for heightened risk of morbidity in COVID-19 patients like asthma, COPD, diabetes, hypertension, high cholesterol, kidney disease, obesity and stroke.

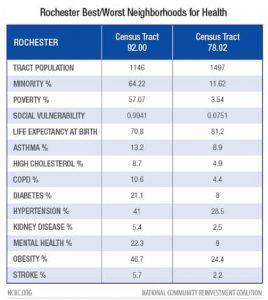

- On average, life expectancy at birth is lower by 3.6 years in redlined neighborhoods, when compared to the neighborhoods graded as the “best” by the HOLC. Differences in life expectancy vary greatly among cities, from 14.7 years less in redlined neighborhoods in Rochester to a 1.3-year greater life expectancy in redlined neighborhoods in Ogden, Utah.

The report’s co-author, Bruce Mitchell, serves as senior researcher for NCRC. He noted several factors which make African American communities more vulnerable for COVID-19. One of those factors is that African Americans often tend to be a larger share of frontline workers.

“African Americans often have more crowded living conditions, greater exposure to air pollution, greater likelihood of being uninsured,” Mitchell said. “And also there are lower percentages of physicians relative to the population share for African Americans. All of these factors come into this increased exposure, or social vulnerability, for COVID-19.”

This is one aspect of structural racism, he said.

“What do we mean by structural racism? This is the totality of ways that society has fostered discrimination through mutually reinforcing inequitable systems,” Mitchell explained. “These are systems in housing that we’re particularly interested in at NCRC, in education, in employment, earnings, benefits, credit availability, the media, healthcare, criminal justice and so on. These are self-reinforcing discriminatory beliefs and values and they affect the distribution of resources, which together affect the risk of adverse health outcomes in communities.”

Rochester’s Empire Justice Center staffers Barbara Van Kerkhove and Ruhi Maker recently co-authored a report on COVID-19 disparities and redlining in Rochester. Maker, who serves as senior attorney for the organization, was part of the October NCRC webinar.

The report, the first in a series of essays accompanying NCRC’s analysis, noted that in June, a group of community leaders in Rochester declared Racism a public health crisis. They urged communities of color to remain vigilant in fighting the spread of COVID-19.

“The groups, La Cumbre and the Greater Rochester Black Agenda Group, linked the disparate impact of COVID-19 on Black and Brown communities to the fact that Black and Latinx people disproportionately suffer from various health conditions that are COVID-19 comorbidities,” the essay stated. “With the new report from NCRC and their academic partners, we know these comorbidities are a direct result of segregation in housing.”

In Rochester, racial segregation began long before HOLC redlining, Van Kerkhove and Maker contend. Rochester was a destination for Black families moving north during the Great Migration, but they were kept out of “respectable” white neighborhoods. Redlining only added to that pre-existing segregation.

“Black families were thus forced to reside in crowded, unsafe housing in parts of what are now the Corn Hill and Upper Falls neighborhoods. This was the tinder that only needed a spark for the July 1964 uprising/rebellion,” Van Kerkhove and Maker wrote.

The uprising didn’t stop racial residential discrimination in Rochester. Neighborhood disinvestment and lack of homeownership opportunities has continually resulted in African Americans not receiving loans, according to the essay.

In 1992, the Empire Justice Center, Melissa Marquez — now CEO of the Genesee Co-op Federal Credit Union — and other nonprofits convened the Greater Rochester community Reinvestment Coalition. The coalition’s first report in the early 90s documented that white low-income households and neighborhoods in Rochester received four times as much lending as middle-income Black households and neighborhoods. Black households were unable to grow their equity due to their inability to get affordable loans, the group found.

“Residential segregation led to racial disparities in public health in Rochester, much like it has in most urban areas in the U.S.,” Van Kerkhove and Maker wrote in their essay. “Children in aging houses were exposed to lead paint. Black and Brown neighborhoods lacked access to fresh foods as grocery stores moved to the suburbs. There are fewer safe and healthy public spaces in segregated neighborhoods.”

Maker in the October webinar said one problem is that banks and lenders aren’t doing enough to help those in redlined neighborhoods escape poverty.

“The banks have designed checking accounts to maximize overdraft fees from the poorest of the poor, while giving free checking to the people who have disposable income,” she said. “We have to serve the Black and Brown communities in New York. They are too large a population for us to just set them aside. I’ve always made it about economics that will help everyone and help the community. If you’re a small bank and you serve Upstate New York, if you don’t do the right thing it will go to hell in a handbasket and your bank will be destroyed.”

The Empire Justice Center report noted that according to the July 15 report of the Monroe County Department of Health, the rate of COVID-19 cases among Black people in the county was four times that of white people and the rate of COVID-19 cases among Latinx people was 2.5 times that of white people. Black and Latinx people are more than twice as likely as white people to die from COVID-19.

Data from the Monroe County Department of Health at the end of July showed that five ZIP codes had the highest rates of COVID-19 per 100,000 residents. The median household incomes in those areas range from $21,000 to $39,000 and their composition is 60 to 88 percent non-white, according to the Empire Justice Center essay.

“The high rates of COVID-19 cases in these five zip codes align with what is being found around the country and with NCRC’s report. They have the highest percentages of people of color and some of the lowest income levels, and all of them are in the city of Rochester,” Van Kerkhove and Maker wrote. “Four of the five zip codes cover most of the census tracts with the highest redlining scores outside of the central business district in NCRC’s redlining map.

“In addition to the impacts of segregation, people who live in formerly redlined neighborhoods tend to work at higher-risk essential jobs, are paid less than a living wage, do not have sufficient health insurance and/or do not have family or sick leave,” they continued. “It is no wonder they have higher COVID-19 infection rates.”

[email protected] / 585-653-4021 / @Velvet_Spicer

n